PEP vs. MEP Retirement Plan Basics

PEPs and MEPs let multiple employers band together in one retirement plan. This guide explains how they work, why employers choose them, common drawbacks, and what doesn’t go away—like Form 5500 responsibilities and potential audit requirements.

Group retirement plans can sound like a win-win: share administrative work, reduce costs, and offer a more “big company” plan experience. Two common ways employers do this are through a MEP (Multiple Employer Plan) or a PEP (Pooled Employer Plan). While both approaches can simplify certain tasks, they also come with tradeoffs—especially around control of plan design and provider selection.

Below are the PEP vs. MEP retirement plan basics plan sponsors and HR teams should understand before joining (or leaving) a group plan.

What is a MEP (Multiple Employer Plan)?

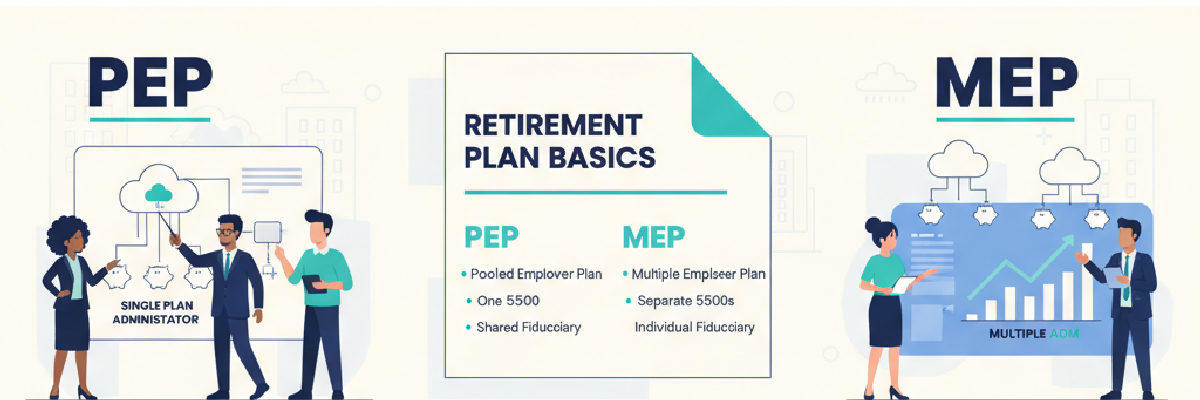

A MEP is a single retirement plan that covers employees of two or more unrelated employers (or sometimes related employers). In a MEP, adopting employers participate under one plan document and a shared administrative structure.

Historically, many MEPs were sponsored by an association or industry group (for example, a trade association). In practice, MEPs vary widely in how they’re run, who makes decisions, and how much flexibility adopting employers have.

MEPs are still subject to ERISA rules and reporting requirements, including annual filings. If you need a refresher on the primary annual filing most plans deal with, see what Form 5500 is and why it matters.

What is a PEP (Pooled Employer Plan)?

A PEP is a type of multiple employer plan created under the SECURE Act framework. The defining feature is that a PEP is run by a Pooled Plan Provider (PPP), which takes on many of the core administrative and fiduciary responsibilities.

In a PEP, the PPP is typically responsible for coordinating key plan operations and hiring/monitoring major service providers. Employers still have responsibilities, but the PEP structure is designed to centralize governance and (ideally) reduce the burden on each adopting employer.

For regulatory background, see the U.S. Department of Labor’s overview of retirement plan rules at EBSA (Employee Benefits Security Administration) and IRS retirement plan resources at IRS Retirement Plans.

Why employers like PEPs and MEPs

Employers typically choose a PEP or MEP for a mix of cost, simplicity, and access to a packaged solution. Common reasons include:

Administrative relief: Many core tasks (plan document maintenance, testing coordination, participant notices, etc.) may be centralized.

Potential cost advantages: Pooling assets and participants can create pricing leverage on recordkeeping and investments—though not always.

More structured governance: Some employers prefer a “turnkey” model with defined roles and fewer vendor decisions to manage.

Fiduciary support (especially in PEPs): The PPP may take on significant fiduciary duties, which can reduce the burden on the adopting employer (but not eliminate it).

Consistency across locations or affiliated groups: For organizations that want a standardized benefit offering, group plans can help.

Even in a group arrangement, employers should understand who is acting as the plan’s fiduciary and how provider oversight works. If you’re weighing whether to bring in outside help for oversight, see how to hire a retirement plan advisor and browse options for 401(k) financial advisors.

Why employers don’t like PEPs and MEPs (the tradeoffs)

The biggest downsides usually come down to control, customization, and transparency. Here are common concerns plan sponsors raise:

You may lose control over provider selection: In many PEPs (and some MEPs), the sponsor/PPP selects the recordkeeper, TPA (third-party administrator), investment lineup, and sometimes the advisor. If you want to choose or change these providers independently, a group plan may feel restrictive.

Less plan design flexibility: Eligibility, match formulas, profit sharing approaches, and other features may be standardized. Some group plans offer limited “menus” of options rather than full customization.

Fee complexity: Pricing can be bundled and harder to compare. Employers should ask for a clear breakdown of all direct and indirect fees.

Service model may not fit every employer: A call-center approach can work well for some workforces and poorly for others.

Transition risk: Moving into or out of a group plan can involve payroll mapping, blackout periods, and participant communication challenges.

If provider control is important to you, it’s worth comparing a PEP/MEP to a standalone plan where you can build your own lineup of partners through retirement plan providers, select your own counsel via ERISA attorneys, and choose your preferred advisory relationship.

Do PEPs and MEPs still need audits and Form 5500 filings?

Yes—joining a group plan does not automatically eliminate annual reporting or audit requirements. The details depend on the plan’s structure and size, but here are the key points:

Form 5500 still applies: Group plans generally file Form 5500 reporting for the plan. Employers should understand what information they must provide to support that filing. Start with what is a Form 5500?

Audits may still be required: If the plan meets the criteria for an annual audit (commonly tied to participant counts under ERISA rules), the plan will need an independent qualified public accountant (IQPA) audit. Learn the basics in what a 401(k) audit is and when you need one.

You may still have employer-level responsibilities: Even if the PPP or MEP sponsor coordinates the audit and filing, adopting employers often must provide payroll data, eligibility info, and contribution support on time.

If you’re facing an audit (or want to be prepared), see what is needed for a 401(k) audit and where to find it. And if you’re worried about missed deadlines or rejected filings, read the high cost of non-compliance for late or rejected Form 5500 audits.

When it’s time to engage an audit firm, you can start with vetted directories like 401(k) auditors (or other plan types such as 403(b) auditors, defined benefit auditors, ESOP auditors, and health & welfare auditors). You can also browse all auditors if you manage multiple plan types.

Other compliance items that don’t go away

Even in a PEP or MEP, certain compliance concepts remain relevant:

Fiduciary responsibility: Employers may still be fiduciaries for certain decisions (for example, choosing to join the PEP/MEP and monitoring that decision over time).

ERISA bonding: Many plans must maintain an ERISA fidelity bond. If you’re unsure what that is, read what an ERISA bond is and how to buy one and explore options through ERISA bond providers.

Payroll and contribution accuracy: Timely, accurate deferrals and employer contributions are still essential—and often still the adopting employer’s responsibility.

How to decide: quick evaluation checklist

Before joining a PEP or MEP, ask these practical questions:

Who selects and can replace the recordkeeper, advisor, and investment lineup? What input do adopting employers have?

What plan design flexibility do we get? Eligibility, match, profit sharing, Roth, auto-enrollment, etc.

What are the all-in fees? Request a clear breakdown (administration, recordkeeping, advisor, investment expenses).

Who handles Form 5500 and the audit? What data must we provide, and by when?

What happens if we want to leave? Understand termination/exit provisions and conversion support.

Conclusion: PEP vs. MEP basics come down to control vs. convenience

A PEP or MEP can be a smart move for employers who want a more packaged retirement plan solution and are comfortable trading some customization and provider choice for centralized administration. The key is going in with eyes open: group plans can simplify governance, but they don’t eliminate compliance—and you may give up control over important partners like advisors and recordkeepers.

If you’re evaluating a group plan or preparing for upcoming reporting and audit requirements, consider lining up the right specialists early—whether that’s an experienced advisor, ERISA counsel, or an independent audit firm.